The 721 Exchange, or UPREIT (Umbrella Partnership Real Estate Investment Trust), offers certain investors a tax-deferral alternative to the traditional 1031 Exchange. This strategy may appeal to clients—especially older investors—seeking to defer taxes, gain liquidity, and diversify through Real Estate Investment Trusts (REITs). As Qualified Intermediaries (QIs), understanding the core mechanics and suitability of the 721 Exchange is crucial to offering clients informed guidance.

What is a 721 Exchange?

The 721 Exchange enables accredited investors to contribute real estate or Delaware Statutory Trust (DST) interests into a REIT, receiving Operating Partnership (OP) units in return. Like the 1031 Exchange, it provides an avenue for tax deferral on capital gains and depreciation recapture. The added benefit of OP units is potential liquidity, giving clients a pathway to move from property ownership into a diversified, passive REIT portfolio. However, this exchange may not suit every investor and requires careful consideration.

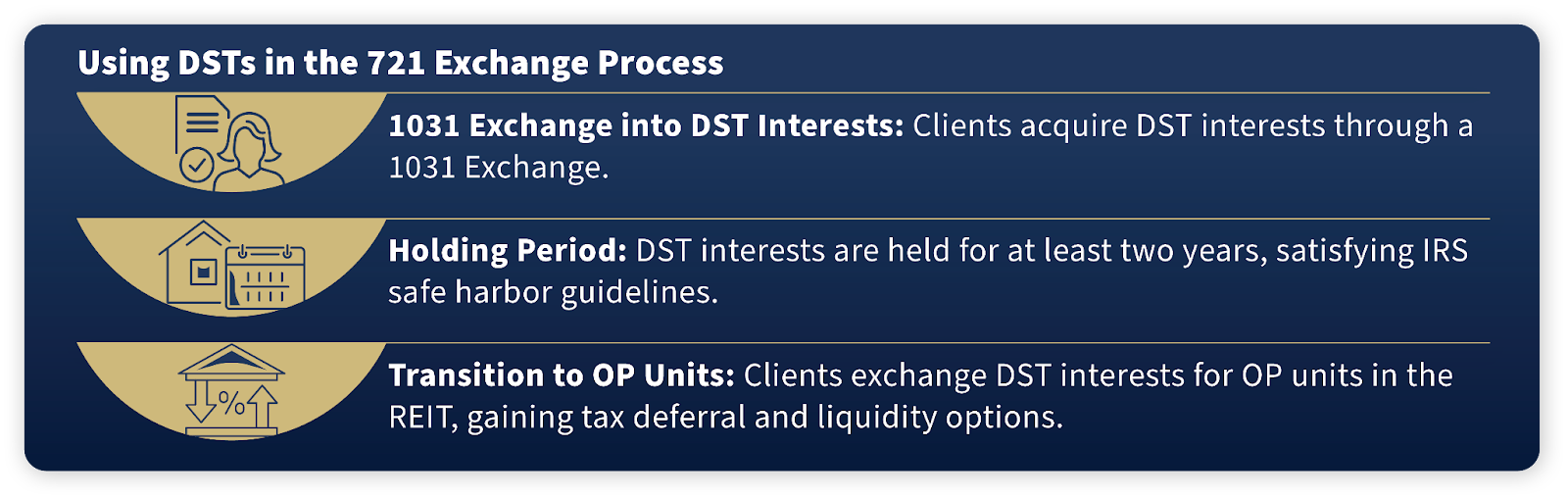

Using DSTs in the 721 Exchange Process

Direct property contributions often don’t align with REIT acquisition criteria, which is where DSTs become valuable. Clients can first acquire DST interests through a 1031 Exchange, then transition to the 721 Exchange once the REIT acquires the DST property. This generally involves:

- 1031 Exchange into DST Interests: Clients acquire DST interests through a 1031 Exchange.

- Holding Period: DST interests are held for at least two years, satisfying IRS safe harbor guidelines.

- Transition to OP Units: Clients exchange DST interests for OP units in the REIT, gaining tax deferral and liquidity options.

Key Benefits for Clients

For appropriate investors, the 721 Exchange can offer:

- Tax Deferral: Clients can reinvest full proceeds without immediate tax liabilities.

- Liquidity: OP units provide potential liquidity post-holding period, allowing redemption for REIT shares or cash.

- Diversification: REITs manage diverse real estate portfolios, potentially reducing concentration risk.

- Estate Planning: OP units or REIT shares often transfer with a step-up in cost basis, reducing capital gains taxes for heirs.

Evaluating Suitability

DSTs offer access to institutional-grade properties across various sectors, including commercial, industrial, and multifamily. This diversification can reduce the risks associated with investing in a single asset class, providing your clients with more stable returns. During periods of economic uncertainty, having a diversified portfolio becomes even more critical.

By incorporating DSTs into their 1031 exchange strategy, your clients can tap into properties they wouldn’t typically have access to, further enhancing their portfolio’s resilience and growth potential.

Limitations to Consider

Clients completing a 721 Exchange cannot use the same capital in future 1031 Exchanges, limiting long-term tax planning flexibility. Additionally, the redemption of OP units for REIT shares can trigger a taxable event, requiring careful timing for tax planning.

Differentiating REITs and UPREITs

It’s helpful to clarify distinctions for clients:

-

REITs: Broadly diversified portfolios of properties, offering passive real estate exposure without direct ownership.

-

UPREITs: Property owners exchange real estate or DST interests for OP units, providing indirect ownership and potential liquidity.

Key Points for QIs

QIs play an essential role in guiding clients through the nuances of the 721 Exchange. Points to consider include:

- No Future 1031 Exchange: This strategy does not allow for 1031 reinvestment with the same capital.

- Liquidity Windows: OP units are redeemable only during specific windows, typically quarterly, after a 12-month holding period.

Conclusion

Offering the 721 Exchange as a tax-advantaged option lets QIs present clients with a diversified, flexible real estate strategy, though suitability must be carefully assessed. To gain deeper insights on how the 721 Exchange might serve specific client needs, download our eBook, “Exploring the 721 Exchange,” for an in-depth guide on navigating this option with precision and clarity.

This is for informational purposes only and does not constitute an offer to purchase or sell securitized real estate investments. Such offers are only made through the sponsors Private Placement Memorandum (PPM) which is solely available to accredited investors and accredited entities.

This material is not to be interpreted as tax or legal advice. Please speak with your own tax and legal advisors for advice/guidance regarding your particular situation.

Because investor situations and objectives vary this information is not intended to indicate suitability or a recommendation for any individual investor.

There are material risks associated with investing in private placements, Delaware Statutory Trusts ("DSTs") and real estate securities including the potential loss of the entire investment principal, illiquidity, tenant vacancies impacting income and revenue, general and real estate market conditions, lack of operating history, interest rate risks, competition, including the risk of new supply coming to market and softening rental rates, general risks of owning/operating commercial and multifamily properties, short term leases associated with multi-family properties, financing risks, potential adverse tax consequences, general economic risks, development risks, long hold periods, and investors should read the PPM carefully before investing paying special attention to the risk section.

Risks associated with 1031 exchange- A 1031 exchange has an identification period of 45 days from the sale of the relinquished property to identify a potential replacement property or properties depending on the value of the previous property. To defer all capital gains tax, you must reinvest the entire net proceeds from the sale of the relinquished property into the replacement property and acquire debt on the new property that is equal to or greater than the debt on the property that was just sold and relinquished.

An UPREIT (umbrella partnership real estate investment trust) is a REIT structure that allows property owners to exchange their property and defer taxes on the sale of property in exchange for UPREIT units though capital gains taxes on UPREIT units are subject to standard REIT taxation. UPREITs are generally subject to Internal Revenue Code (IRC) Section 721 exchanges.

Securities offered through Concorde Investment Services, LLC (CIS), member FINRA/SIPC; Advisory services offered through Bangerter Financial Services, Inc., a state registered investment advisor. Insurance offered through Concorde Insurance Agency, Inc. (CIA). Bangerter Financial Services, Inc. is independent of CIS and CIA.

ia-sb-r-a-228-11-2024

.png?width=273&height=103&name=Brokercheck%20(1).png)

Comments